The main economic problems of society: what to produce? how to produce? for whom to produce?; their solution in various economic systems. Market economy - what, for whom, how to produce is decided by the manufacturer himself, focusing on the ratio of demand

The main task of the economy is to use economic resources in order to obtain an economic product (material goods, works, services). An economic product serves the purpose of satisfying the needs of all economic entities. Few goods are available in such large quantities that they do not require choice on the part of subjects.Such characteristic properties of needs as unlimitedness, insatiability, continuous growth in quantitative and qualitative terms indicate the impossibility of establishing a reasonable limit for their satisfaction.

Of course, some needs of an individual may well be fully satisfied. Even if we imagine that this specific need in a given period is completely satisfied, then in this case it is obvious that all other simultaneously existing needs of the subject remain unsatisfied. This is especially true for collective, social, and state needs, the specific limits and levels of full satisfaction of which are unattainable.

50 Section I. Basics

Choice is necessary because we live in a world of scarcity. Scarcity means that human needs are unlimited and the resources available to satisfy them are limited. But is it correct to talk about unlimited human needs? A person may think that at the moment he only wants to have a few things: a car, a new CD player and a comfortable apartment. However, let’s imagine that next week he wins 100 million rubles. As an individual with selfish interests, the lucky one will rush to buy a car, a CD player, etc. But now he can afford a vacation at an expensive resort, give gifts to family and friends, set aside savings in order to live on annual interest for many years. He can spend some amount of money on charity.

So, although the list of needs for most people is unlimited, they could make a reasonably long list of desirable goods and services of all kinds of better quality, and also include in it some needs that are not personal or selfish.

Subjects would like to consume an almost unlimited amount of the final economic product in the form of consumer goods and services. Their production requires an even greater quantity and structural diversity of intermediate products (factors of production), the production of which requires the use of economic resources.

The means that a person has to satisfy his needs are either insufficient at the moment or are irrationally distributed in the economic space. Even if a person had excess material resources, even then he would be limited in the consumption of such an important resource as time. In addition, the subject cannot take advantage of all the benefits at the same time, since many of them are mutually exclusive. People must distribute the funds they have due to the finiteness and limitations of the latter. Money can be spent in many ways.

On the one hand, the volume and degree of replenishment of stocks of various goods characterizes their relativity in relation to each other and is expressed in the concept of rarity. On the other hand, the limitation of goods relative to the needs for them is expressed by the concept of insufficiency. We are talking about two sides of limited goods. And the limited nature of consumer goods, resources and technologies is a universal property of economic goods.

To achieve any goal, a subject (individual or collective) is forced to sacrifice his other goals or use limited means and scarce time. Therefore, any economic choice is accompanied by

51

is driven by sacrifice, the price of which the French economist R. Barr called the price of adaptation. It is the real cost of the sacrifice made by an economic actor choosing between several possible actions.

Firms face problems of profit distribution, hiring workers, purchasing equipment, purchasing raw materials, etc. On the scale of the national economy, society faces the need to distribute national income for various purposes (investments, social security, etc.) -

Thus, any economic entity invariably makes a choice of one of mutually exclusive solutions. The need for this is due to the limited nature of goods and the impossibility of their simultaneous consumption and use. All of the above forms of limited benefits presuppose the emergence of a choice problem (Fig. 2.5).

Rice. 2.5. The problem of choice in economics

The problem of choice is universal; it does not depend on the type of economic system. Economics, or economic theory, in its most general form, is the science of how people make choices in a world of scarcity. Everything that has value is rare - money, goods, time, human abilities. At the same time, human desires are almost unlimited. Since the resources needed to satisfy the endless demands for goods and services are limited, choice is not a theoretical assumption, but a reality of life.

At the level of the economy as a whole, society must decide what to produce, how to produce it, and for whom (we already discussed this in Chapter 1). Each society answers these questions differently. The difference in the approach to the allocation of resources in different economic systems, however, demonstrates a common mechanism for solving the problem of choice and overcoming the scarcity of resources. In economic theory, resource allocation is understood as their placement based on finding the optimal way to distribute limited goods.

52 Section I. Basics

In the conditions of primitive communal production, the individual produced the products necessary for consumption with his own labor, independently deciding on the distribution of natural resources, tools and time that were required for hunting, fishing, etc. Within the framework of subsistence farming, the peasant produced as much as was necessary to satisfy his own needs and the demands of his family.

In modern conditions, isolated activity in the “man-nature” plane is impossible. Even in the simplest production there is a separation of functions. The emergence of the division of labor (specialization of individuals in performing certain operations) led to the separation of producers and consumers. An objective need for economic coordination has emerged, i.e. coordination of the activities of economic entities, plans and actions of various individuals. Moreover, a change in the economic behavior of one individual may require a change in the behavior of others. The economy is social, and its functioning is determined by the needs, plans and actions of many subjects, each of which depends on the needs, plans and actions of others.

Deciding what to produce depends indirectly on the desires of the end consumer. Individuals, specializing in the production of one good, obtain other necessary goods through exchange.

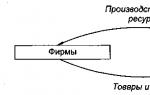

Modern society consists of households, i.e. subjects who, on the one hand, consume goods and services, and on the other, offer resources and factors for the production of economic goods. In addition to them, society is represented by firms - organizations that decide what goods and services to produce. Based on the decisions they make, they use the resources offered by households (Figure 2.6).

Resources are limited, but society wants to use them to achieve the maximum possible satisfaction of needs. The presence of a choice problem means that certain relationships must exist between households and firms. The social connection through which the needs of households and firms are coordinated reveals the content of the mechanism for coordinating economic behavior, or the coordination mechanism.

One of the ways that determines economic behavior is through price changes. An increase or decrease in the price of a particular product can occur under the influence of supply and demand or be the result of directive planning.

The mechanism for coordinating economic behavior includes solving previously formulated problems: what, how and for whom to produce?

“What to produce” is the problem of determining the range and volume of products produced by firms in a certain period of time.

“How to produce” is a problem of methods of organizing production and choosing technology.

“For whom to produce” is the problem of determining the subjects who will buy the selected goods and services and become consumers of the products.

Coordination mechanisms in any economic system must resolve these issues so that the system avoids internal contradictions and instability in its development.

In modern economics, two coordination mechanisms can be distinguished: hierarchy and spontaneous order.

Management within a company, any economic organization, the state apparatus and the entire national economy (administrative command system) is based on hierarchical subordination.

Spontaneous order corresponds to the market organization of economic activity. When making decisions, economic entities are guided by market signals. Focusing on price movements, consumers and producers strive for personal gain. In this case, complete coordination of actions and an increase in social welfare are achieved. The above corresponds to A. Smith’s idea of the “invisible hand of the market”: the actions of a person striving for personal gain, as if by an invisible hand, are directed in such a way that they serve the interests of society more fully than if the person consciously sought to serve them.

1. Main economic issues

Each society, faced with the problem of limited available resources with an unlimited growth of needs, makes its own choice and answers the three main questions of economics in its own way.

What to produce? How to determine priorities in meeting needs, which goods and in what quantity should be produced?

How to produce? How to use available resources most effectively, what resources to attract, how to organize production?

For whom to produce? How to distribute produced goods, who will receive them and on the basis of what principles?

Depending on how society answers the main questions of the economy, certain types of economic systems emerge: traditional, market, centralized.

An economic system is a way of organizing the joint activities of people in society. The concept of an economic system includes such decision-making mechanisms as the legal system, forms of ownership, moral norms, habits, customs accepted in a given society.

2. Types of economic systems

In a traditional economic system, the three main questions of economics (what to produce? how to produce? for whom to produce?) are resolved in accordance with established traditions. Examples of observed traditions in the economy are: customary farming methods, norms of consumption of certain products, religious prohibitions on the production and consumption of specific goods, etc. Sales and purchase relations are poorly developed, agriculture predominates.

Most of the history of human development took place within the framework of the traditional economic system.

O Remember from the course of general history what forms of social

development corresponds to the traditional economic system.

The main incentive for economic activity under the traditional system is the desire to survive. The advantages of this system are predictability and stability. Serious disadvantages include a low standard of living, lack of progress and economic growth.

A centralized system, which is also called a planned, administrative, command system, is characterized by the fact that state ownership is the main form of ownership. Three main issues are decided by central government agencies. These decisions are reflected in state plans and take the form of directives (orders), which are binding on all enterprises. Centralized regulation is carried out not only in the sphere of production of goods, but also in the sphere of their distribution. Such an economic system was implemented in the Soviet Union and, partly, in the countries of the socialist community. The centralized solution of the main economic issues in the USSR made it possible to achieve success in the natural sciences, space exploration, ensure the country's defense capability, create powerful social protection systems, etc.

However, the command-administrative economic system of the USSR turned out to be unable to ensure the development of personal initiative. One of the principles of a command economy is the principle of equal distribution. If an enterprise managed to make a large profit, then almost all of it was confiscated and transferred to the state budget. Workers received almost the same wages; incentives for highly qualified, creative work were insignificant and had not so much a material as a moral basis. All this gave rise to the enterprise’s disinterest in improving production technology, increasing productivity, and the lack of personal interest of people in the results of their work. Gradually, the USSR began to lag behind the leading powers of the world community in the most important socio-economic indicators. The suppression of economic independence of economic entities led to a deterioration in the quality of economic growth and its slowdown. There was a need for radical reform of the economic system.

Market system. In a market system, the role of government is limited. The main subjects of market relations are economically independent participants in economic activity: citizens and firms. Their interaction takes place on the market. A market is any form of contact between sellers and buyers on the basis of which purchase and sale transactions are made. There are many types of markets; they are classified according to the economic purpose of the objects, by geographical location, and by industry.

Markets are in constant interaction, forming a single complex system.

The basis of the market mechanism is individual freedom in making and implementing economic decisions. Freedom of choice in a market economy is enjoyed by entrepreneurs, resource owners and consumers.

Enterprises have the right to purchase factors of production at their own discretion, produce those goods and services that they consider necessary, and choose the method of their production; In this case, decisions are made at your own expense, at your own risk.

Resource owners can use resources at their own discretion. This also applies to the owners of labor resources; they can engage in any type of work that they are capable of.

Consumers can buy the goods and services they want within the limits of their income. In a market economy, the consumer occupies a special position; it is he who decides what the economy should produce; If the consumer does not want to buy goods and services, then the firms will go bankrupt.

The main form of ownership of factors of production is private. Private property assigns to a person the rights to own, use and dispose of economic goods or resources.

Remember from your social studies course what property is.

The main issues of the economy in a competitive environment are resolved on the basis of a system of free prices under the influence of market information.

The question “what to produce?” decided by firms taking into account consumer demand.

The question “how to produce?” is decided by firms taking into account the profitability motive, i.e. firms choose the most efficient method of production.

The question “for whom to produce?” is decided in accordance with the solvency of buyers.

The main incentive for enterprises to operate in a market system is profit. The advantages of a market economy are more efficient use of resources, system mobility, its ability to adapt to changes, and the introduction of new technologies. But the market system has a number of shortcomings, so-called market “failures,” which we will consider below.

|

All types of economic systems can be represented in the form of a diagram.

In real life, all countries have a mixed economic system, which combines the features of other systems: traditional, centralized and market. Depending on their predominance, a mixed economy of traditional, centralized or market type is distinguished.

3. Mixed economic system

In a market economy, problems arise that the market system cannot solve. Such cases of market failure are: inflation, unemployment, the emergence of monopolies, cyclical development of the economy, uneven distribution of income of citizens.

In a market system, the need to produce public goods also arises. Public goods are economic benefits, the use of which by some members of society does not exclude the possibility of their simultaneous use by other members of society. These include, for example, national defense, fire protection, emergency response (earthquakes, floods), state television and radio broadcasting, etc. Public goods differ from private goods, which have a private seller and a private buyer, in such properties as non-competitiveness, non-excludability and non-profitability. Non-competitiveness means that goods and services can be

used by many people at the same time; at the same time, the quantity of goods available to others does not decrease (for example: lighthouse, fireworks). Non-excludability is the impossibility of excluding those who do not pay for them from using these services, the so-called “rabbit effect”, for example national defense or street lighting. Hence the non-profitability of public goods, the unattractiveness of their production for commercial firms (for example: firefighters, emergency rescue services.

|

Moreover, the market is unable to solve the problem of externalities. Externalities are positive or negative impacts on those who do not participate in the production or consumption of a given good.

Examples of a positive external effect: a free bus to the supermarket - for local residents, a good road to a rich mansion - for everyone who will use this section of the road.

Examples of a negative external effect: environmental pollution by an enterprise, smoking in public places, etc.

Both positive and negative external influences reduce the efficiency of resource use, since in both cases the price of the product is underestimated. At the same time, the quantity of goods sold is artificially low in the case of a positive external effect and unjustifiably inflated in the case of a negative external effect. In the topic of market equilibrium, we will return to this issue and analyze specific situations with externalities.

The presence of market failures necessitates government intervention and the formation of a mixed economic system. In mixed

system, private and public organizations jointly exercise economic control.

Currently, Russia has a mixed market economy.

Three main questions of economics:

What to produce?

How to produce?

For whom to produce?

Depending on how society answers the main questions, a certain type of economic system is formed: traditional, command or market.

The presence of market failures necessitates government intervention and the formation of a mixed system.

Basic Concepts

Economic system Main issues of economics Traditional system Centralized system Market system Market

Private property Mixed system Market failures.

Public goods

External effects

Questions and tasks

1. What is an economic system?

2. Name the three main issues of economics. Why does every society have to deal with these issues?

3. How are the main issues resolved in the traditional system?

4. Which form of ownership is the main one in a centralized system, and which is the main one in a market system?

5. What forces firms to produce quality goods in a market economy? Explain why.

6. Give examples of market failures.

7. What characterizes the modern economy in Russia as an economy of a mixed market type?

8. What are public goods and services? Why don't companies produce them?

9. “Either power or the ruble - there has not been and is no other choice in the economy since the ages, from Adam to the present day.” How do you understand this statement by N. Shmelev?

Economic choice and production possibilities frontiers

In general, economic relations between people characterize their property status in society.

Economic relations and their structure

Interaction of people in economic life

Economic relations between people

The result of the interaction of production factors is the creation of goods

Economic activity of people presupposes the presence of social connections.

These connections are significantly influenced by property relations, since behind them are the economic interests of both individuals, groups, and society as a whole.

Economic interest - this is an incentive, a stimulus for human economic activity in any direction.

Among the huge number of facts, phenomena, and connections of an objective nature, one can single out the most significant, predetermining actions and development of many economic processes and even the economy as a whole. They are usually called economic laws.

Economic law – these are objectively necessary, stable and massively repeated connections and interdependencies between phenomena and processes occurring in the economic activities of people.

Objective economic laws represent the core of economic relations.

Economic relations – relationships between people that arise in the process of production, distribution, exchange and consumption of material and spiritual goods and services.

There are three groups of carriers of economic relations in a market economy:

a. producers and consumers;

b. sellers and buyers;

c. owners and users of goods.

Any country, developing production, is forced to pose three fundamental questions:

1. what goods to produce,

2. how to produce them

3. Who should I do this for?

In a market economy, the producer sets himself the goal of obtaining the maximum possible income, selecting for production the most suitable material goods for this purpose. This is the answer to the first question: what to produce?

Having decided on the range of goods to be produced, firms in a market economy choose those technologies that provide the lowest production costs. Thus, the market provides an answer to the second fundamental question of economics: how to produce goods and services?

The population, having monetary income, which is also a limited consumer resource, compares the prices of different goods and tries them on to their own capabilities, chooses what to buy and at what price. Therefore, in a market economy, goods are produced for the consumer.

The main economic task is to choose the most effective option for the distribution of production factors in order to solve the problem of limited opportunities, which is caused by the unlimited needs of society and limited resources. Given information about its production capabilities, any society must find answers to the following three questions.

— What goods and services should be produced and in what quantity?

— How should these goods and services be produced?

— Who will buy and be able to consume (use) these goods and services?

- What to produce?

An individual can provide himself with the necessary goods in various ways: produce them himself, exchange them for other goods, receive them as a gift. Society as a whole cannot have everything immediately. Because of this, it must decide what it would like to have immediately, what it can wait to get, and what it can refuse altogether.

Developed countries, for example, put a lot of effort into improving the production of a limited range of goods in order to achieve some success in competition with other countries. These could be cars, computers or other goods.

Sometimes the choice can be very difficult. The so-called "underdeveloped countries" are so poor that the efforts of most of the workforce are spent just feeding and clothing the country's population. In such countries, living standards can be raised by increasing production. But since the labor force is fully employed, it is not easy to increase the level of social production. It is possible, of course, to modernize the equipment in order to increase production volume. But this requires a restructuring of the national economy. Some resources will be switched from the production of consumer goods to the production of capital goods, the construction of industrial buildings, and the production of machinery and equipment. Such a restructuring of production will reduce the standard of living in the name of its future increase. However, in countries with low living standards, even a slight decrease in the output of consumer goods can push a large number of people to the brink of poverty.

How should goods and services be produced?

There are different options for producing the entire set of goods, as well as each good separately. By whom, from what resources, using what technology should they be produced? Through what organization of production? For different projects, you can build an industrial and residential building, for different projects you can produce cars, or use a plot of land. The building can be multi-story or one-story, a car can be assembled on a conveyor belt or by hand, a plot of land can be sown with corn or wheat.

Some buildings are built by private individuals, others by the state (for example, schools). The decision to build cars in one country is made by a government agency, in another - by private firms. The use of land can be carried out either at the request of farmers, or with the participation or decision of government agencies.

Who is the product made for?

Since the number of goods and services created is limited, the problem of their distribution arises. Who should use these products and services and derive value? Should all members of society receive the same share or should there be poor and rich, what should be the share of both? What should be given priority - intelligence or physical strength? The solution to this problem determines the goals of society and the incentives for its development.

As is known, an economic system is a set of interconnected and ordered elements of the economy in a certain way.

Without the systemic nature of the economy, economic relations and institutions could not be reproduced (constantly renewed), economic patterns could not exist, a theoretical understanding of economic phenomena and processes could not have developed, and there could be no coordinated and effective economic policy.

Real practice constantly confirms the systemic nature of the economy. Objectively existing economic systems are scientifically reflected in theoretical (scientific) economic systems.

as the history of economic science shows, the classification of economic systems can be made on the basis of various criteria (features). This multiplicity is based on the objective diversity of properties of economic systems.

In an enlarged form, the criteria of economic systems can be divided into three groups: structure-forming criteria; socio-economic (substantive) criteria; volumetric and dynamic criteria.

It is the totality of all economic processes occurring in society on the basis of the property relations and organizational forms operating in it that represents economic system this society.

Human society in its development has used and continues to use various economic systems. They differ in their approach and methods of solving basic economic problems.

Traditional systems

Some so-called “underdeveloped countries” have traditional, customary economic systems. Traditions passed down from generation to generation determine what goods and services are produced, how and for whom. The list of goods, production technologies and distribution are based on time-honored customs. The economic needs of individuals are determined by heredity and caste. Technical progress penetrates these systems with great difficulty, since it conflicts with traditions and threatens the stability of the existing system.

The presence of specific resources also determines traditionalism in solving economic problems. For example, if Brazil grew mainly coffee last year, then this year it will grow coffee, using the same technological methods, and for the same importing consumers.

Command economy

All decisions on major economic issues are made by the state. All resources here are the property of the state. Central economic planning covers all levels - from household to state. Resource allocation is based on long-term priorities. Because of this, the production of goods is constantly divorced from social needs. The progress of society is hampered.

Market economy

“What” is decided by effective demand, by voting with money. The consumer himself decides what he is willing to pay money for. The manufacturer himself will strive to satisfy the consumer’s desire to pay money for the product he needs.

The “how” is decided by the manufacturer seeking greater profits. Since setting prices does not depend only on him, in order to achieve his goal in a competitive environment, the manufacturer must produce and sell as many goods as possible and at a lower price than his competitors.

“For whom” is decided in favor of different consumer groups, taking into account their income.

Mixed economy

The modern market system is a combination of forms of entrepreneurial activity and the role of the state. Let us illustrate this using the example of the economies of some developed countries.

The Swedish system is characterized by strong state participation in ensuring economic stability and in income redistribution. The core of the Swedish system is social policy. For its successful implementation, a high level of taxation has been established, which amounts to more than 50% of the gross national product. As a result, unemployment in the country has been reduced to a minimum, differences in the incomes of different groups of the population are relatively small, and the level of social security for citizens is high. The export capacity of Swedish companies is also high. The main advantage of the Swedish model is that it combines relatively high rates of economic growth with high levels of full employment and well-being of the population.

The Japanese economic model is characterized by advanced planning and coordination between the government and the private sector. Economic planning of the state is advisory (indicative) in nature. Plans are government programs that orient and mobilize individual parts of the economy to accomplish national goals. The Japanese economy is characterized by the preservation of national traditions while borrowing from other countries everything that is needed for the development of the country. This makes it possible to create management and production organization systems that are very effective in Japanese conditions. Borrowing Japanese experience from other countries does not always give the expected result (for example, quality circles), since these countries do not have Japanese traditions.

In the American economy, the state plays an important role in developing and enforcing the rules of the economic game, ensuring R&D, freedom of enterprise, and developing education and culture.

A mixed economy dictates the most efficient use of resources and promotes the development and use of advanced technologies. An important non-economic argument in favor of a mixed economy is its emphasis on personal freedom. Entrepreneurs and workers move from industry to industry by their own decision, and not by government directives.

Societies with different historical and cultural heritage, different customs and traditions use different approaches and methods for effectively using their own resources.

2. SOCIO-ECONOMIC CONSEQUENCES OF INFLATION. ANTI-INFLATION POLICY OF THE STATE

As an economic phenomenon, inflation has existed for a long time. It is believed that its appearance is associated almost with the first period of the emergence of money. The very concept of “inflation” (from the Latin inflatio - inflation) first began to be used in North America in 1861–1865. It meant a certain process leading to an increase in paper money circulation. Soon this concept began to be used in Great Britain and France, mainly among financiers and bankers. It appeared in economic literature at the beginning of the 20th century.

Inflation is a socio-economic phenomenon that is generated by imbalances in various spheres of the country’s market economy; it has still not been fully covered scientifically. Inflation is the most acute problem of modern economic development, therefore it requires, first of all, clarification as a socio-economic concept.

The disorder of the laws of monetary circulation is most often explained by the action of external factors. As a rule, in most cases of inflation there is opposition to the monetary side of factors located in the sphere of production. Violation of a number of national economic proportions in the sphere of production and circulation leads to a violation of the conditions of exchange. The essence of the inconsistency and violation of the terms of exchange is that for each subsequent buyer the same monetary value is exchanged for an ever smaller commodity equivalent.

Inflation can be considered as a manifestation of contradictions occurring as a result of rising prices and depreciation of monetary units, on the one hand, between real and monetary capital, and, on the other, between real and fictitious capital. In other words, emerging structural imbalances in the reproduction of social capital ultimately lead to higher prices.

In domestic literature, the word “inflation” is most often identified with the establishment of a new equilibrium of supply and demand in changing conditions. Often, when determining inflation, it is made dependent on the interpretation of such economic categories as demand, supply, and equilibrium. In particular, inflation is considered to be an excess of the amount of money in circulation in relation to the cost of goods and services (at a given money turnover rate), leading to their depreciation.

Under the conditions of a totalitarian regime, in a socialist economy, the phenomenon of inflation was not “noticed.” It was believed that since the amount of money in circulation is established systematically in accordance with the needs of retail trade turnover, inflation cannot arise. It did not take into account that inflation can be hidden, manifested in commodity shortages. It was precisely this reason that the reduction in production volume aggravated inflationary processes in 1990. The peculiarity of the economic crisis in Russia was that it was not accompanied by a fall in the incomes of enterprises and the population, which aggravated inflation.

The following explanations for the occurrence of inflation do not bring anything new:

the fall in the purchasing power and value of money, its value for subjects of the economic process;

reduction in the real “weight” of cash income and expenses;

For the Western economy, the formula “inflation - rising prices” turned out to be unacceptable, because “there” inflation means rising prices while maintaining a balance between supply and demand. The most popular textbook in the West by K. McConnell and S. Brew, “Economics,” states that “inflation is an increase in the general price level.” This, of course, does not mean that all prices necessarily increase. Even during periods of fairly rapid inflation, some prices may remain relatively stable while others fall—one of the sore points of inflation is that prices tend to rise very unevenly. Some jump, others rise at a more moderate pace, and others do not rise at all.

So, for the West, the main thing in this issue is prices, their general level. In Russia, the concept of inflation is also associated with prices, but from a different perspective: the population has money, but there is nothing to buy - this was the result of price liberalization. The concept of inflation in Russia has its own properties and does not fit into the framework of the classical concept. The concept of an inflationary situation, when effective demand exceeds the supply of goods and services, applies not only to the consumer market, but also to the market for industrial and technical products. Hence the popular definition of inflation: the overflow of monetary circulation with paper banknotes and their depreciation, i.e. the excess of the number of banknotes over the commodity collateral in circulation.

In all cases, inflation should be considered as: a violation of the laws of monetary circulation, which causes a disorder in the state monetary system; obvious or hidden price increases; naturalization of exchange processes (barter transactions); decline in living standards of the population.

The consequences of inflation are diverse, contradictory and are as follows.

Firstly, it leads to the redistribution of national income and wealth between various groups of society, economic and social institutions in an arbitrary and unpredictable manner.

Secondly, high rates of inflation and sharp changes in the price structure complicate planning (especially long-term planning) for firms and households. As a result, the uncertainty and risk of doing business increases. The price for this is an increase in interest rates and profits. Investments begin to be short-term in nature, the share of capital construction in the total volume of investments decreases and the share of speculative operations increases. In the future, this may lead to a decrease in the nation's welfare and employment.

Thirdly, the political stability of society is decreasing and social tension is increasing. High inflation facilitates the transition to a new structure of society.

Fourthly, relatively higher rates of price growth in the “open” sector of the economy lead to a decrease in the competitiveness of national goods. The result will be an increase in imports and a decrease in exports, an increase in unemployment and the ruin of commodity producers.

Fifth, the demand for more stable foreign currency is increasing. Capital flight abroad and speculation in the foreign exchange market are increasing, which in turn accelerates price growth.

Sixth, the real value of savings accumulated in cash decreases, and the demand for real assets increases. As a result, prices for these goods rise faster than the general price level changes. Accelerating inflation spurs growth in demand in the economy and leads to a flight from money. Firms and households have to incur additional costs to purchase real assets.

Seventh, the structure of the state budget is changing and real revenues are decreasing. The state's ability to pursue expansionary fiscal and monetary policies is narrowing. The budget deficit and public debt are increasing. The mechanism of their reproduction is launched.

Eighth, in an economy operating under conditions of underemployment, moderate inflation, slightly reducing the real income of the population, forces it to work more and better. As a result, creeping inflation is both a “payment” for economic growth and a stimulus for it. Deflation, on the contrary, leads to a decrease in employment and capacity utilization.

Ninth, in conditions of stagflation, a high level of inflation is combined with high unemployment. Significant inflation does not provide an opportunity to increase employment. However, there is no direct relationship between inflation, on the one hand, and production volume and unemployment, on the other.

Tenth, there is a multidirectional movement of relative prices and production volumes of various goods.

According to the "accelerating inflation" theory, over the long term, rising inflation rates from year to year help maintain real output above its natural level.

For anti-inflationary regulation, two types of economic policies are used:

policies aimed at reducing the budget deficit, limiting credit expansion, and curbing money emission. In this case, a monetarist approach is used - regulating the growth rate of the money supply within certain limits (in accordance with GDP growth);

a policy of regulating prices and incomes, which aims to link rising wages to rising prices. One of the means is income indexation, determined by the level of the subsistence minimum or the standard consumer basket and consistent with the dynamics of the price index. To curb undesirable phenomena, limits may be set on increasing or freezing wages and limiting the issuance of loans.

An active fight against inflation, called deflationary policy, usually leads to a drop in GDP growth rates and even a contraction (deflation).

What, how and for whom to produce? The answers to these three questions must be found by every country and society that wishes to effectively use all the resources at its disposal. The difficulty of making decisions on these issues is associated with objective restrictions and the need to make choices: after all, resources are limited and there are opportunity costs. This applies to all societies, regardless of their political system and level of development. The only differences between countries are in the methods of distribution.

Fundamental economic questions of “what, how, for whom to produce” are resolved at the micro and macro levels. They arise in societies with any type of economy. Explanation: needs are limitless, but resources are limited and rare. This gives rise to problems of choice: what, how and for whom to produce

Society always strives to effectively use all the resources at its disposal. To do this, he needs to find answers to the questions of what, how and for whom to produce.

The question “what to produce?” arises due to the fact that resources are limited, there is a possibility of choice and there are opportunity costs. The question of what to produce is fundamental to any society.

The second question is “how to produce?” arises because each country, regardless of what technological level it is at, has at its disposal relatively cheap and relatively expensive resources. For example, India has a labor surplus (so labor is cheap) and a capital shortage (capital is expensive). The United States has relatively cheap capital and expensive labor. Society is always interested in creating the desired set of goods and services at minimal cost.

The third question, “for whom to produce?” is, of course, the most difficult, since it reflects society’s attitude towards justice and economic equality. The whole of society must somehow decide what it considers a fair distribution and then choose a way to achieve that distribution. In practice, moving towards equitable distribution may mean a partial abandonment of efficiency. Society must decide how much efficiency it is willing to sacrifice in the name of a more equitable distribution.

The difficulty of making decisions on these issues (what, how and for whom) is associated with objective constraints and the need to make choices. This applies to all societies, regardless of their political system and level of development. The only differences between countries are in the methods of distribution.

So a reflection of this problem is the formulation of three main questions of economics:

what to produce, which of the possible goods and services should be produced in a given economic space and at a given time;

how to produce, with what combination of production resources, using what technologies the goods and services selected for production should be produced;

and since the quantity of created goods and services is limited, the problem of their distribution arises or the third question - for whom to produce, who will consume the goods produced?

These three questions are usually simply formulated as: “what, how and for whom.”

The answers to these questions depend on the economic system existing in society. An economic system is a set of organizational mechanisms through which limited resources of society are distributed to meet people's needs. The nature of the economic system depends on the form of ownership of production factors and on the mechanism for coordinating the actions of economic entities.

Different economic systems answer basic economic questions differently.

Traditional economy is an economic system based on private property, in which traditions, customs, and experience determine what to produce and how to use production resources. The traditional economy was characteristic of medieval Western Europe; today such an economic system exists in some underdeveloped countries. The structure and production technology are inactive. Technological progress penetrates such systems with great difficulty, as it conflicts with traditions.

Command (planned) economy - answers to all basic economic questions are provided by the state. All resources are owned by the state, and it is the state that distributes resources between industries and enterprises, determining what to produce and in what ways, and how to distribute the goods produced. All of these decisions are made based on predetermined, long-term production plans. The inflexibility of such a system in conditions of mobility of needs leads to a constant separation of production from needs.

A market economy is an economic system based on private ownership of factors of production and on decisions made by individual economic entities - individuals and firms - independently, independently of each other. Independent decisions of individual economic entities are coordinated by the market. The market provides answers to basic economic questions.

Mixed economy. It should be noted that the market system does not exist in its pure form. In every, even the most “trade-market” economy, the state performs certain regulatory functions, taking part in solving basic economic problems. In modern conditions, the state often takes upon itself the production of products that are unprofitable for private business, but necessary for society; by in every possible way stimulating scientific and technological progress, it influences the choice of production methods; By solving social problems, it adjusts the market distribution of income. Thus, most developed countries today are characterized by a mixed economy, which is regulated by the market mechanism and the state.

Along with established, established economic systems, today in the world there are countries with transition economies - economic systems that are characterized by the presence of both old economic forms and elements of new, as well as mixed (transitional) forms and relations. A clear example of a transition economy is the economy of former socialist countries, including Russia, which are making the transition from a planned to a mixed economy.